Interest Rates, the Fed, and You

The Federal Reserve is mentioned often in headlines, usually in the same breath as “inflation,” “unemployment,” or “interest rates” - and this year, Fed Chair Jerome Powell’s term comes to a close. Although we mentioned this briefly in our January market outlook webinar, it’s worth taking a closer look at what the Fed does, why leadership changes matter, and what - if anything - this means for long-term investors like you and me.

Federal Funds Rate: The “Wholesale” Price of Money

One of the Federal Reserve’s primary responsibilities is setting the Federal Funds Rate. In simple terms, this is the interest rate that banks charge one another to borrow money overnight.

Banks are required to hold a certain amount of cash in reserve at the Federal Reserve to ensure they can meet customer withdrawals. If a bank ends the day with excess reserves, it can lend to another bank that is temporarily short. Because of this central role in the banking system, the Federal Reserve is sometimes referred to as “the bankers’ bank.”

Though the Federal Funds Rate is set for banks, it also influences short-term rates and borrowing costs throughout the entire economy, affecting mortgages, car loans, and credit cards. When the Fed raises rates, it is generally attempting to moderate inflation or cool an overheating economy. Higher rates make borrowing more expensive and can slow spending and investment. When the Fed lowers rates, it is typically aiming to support economic growth and employment by making borrowing more affordable. The Fed may also hold rates steady when conditions suggest stability is appropriate.These decisions are made by the Federal Open Market Committee (FOMC), a group within the Federal Reserve which meets eight times per year to evaluate economic conditions and determine this incredibly influential number.

Independence: Why does it matter?

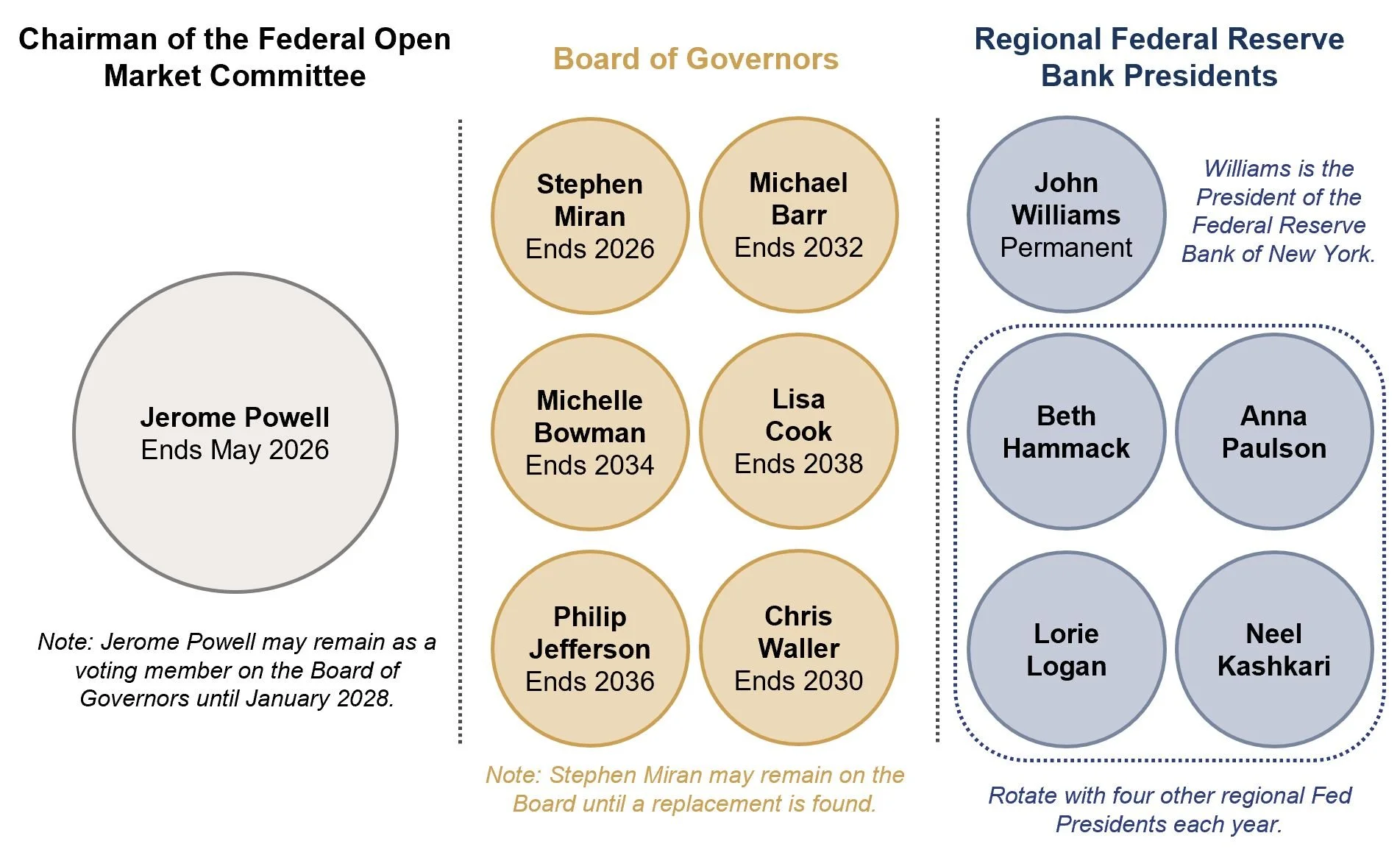

So who are the people that make such far-reaching policy decisions? Looking at how significant the Federal Funds Rate is, it’s natural to be curious about what checks and balances exist to maintain the Fed’s independence. The FOMC includes twelve voting members: the seven members of the Board of Governors and five of the twelve regional Federal Reserve Bank presidents.

Source: Rothschild & Co.

Members of the Board of Governors, including the Chair, are nominated by the President, confirmed by the Senate, and directly accountable to Congress. The current Federal Reserve Chair, Jerome Powell, was nominated in 2018 by President Trump.

Regional presidents are selected through an internal process rather than by the White House, though the Board of Governors must sign off on their appointment. This system is designed to keep their selection independent of the government (provided the Board of Governors itself remains a non-partisan body).

Why does this matter? The FOMC’s decisions on monetary policy might concern banks most directly, but the effects ripple through the U.S. economy and make a difference in our daily lives. The Federal Funds Rate affects rates on your savings accounts, credit cards, auto loans, mortgages and more. On top of this, the U.S. stock market and investor sentiment is heavily influenced by the Federal Reserve’s policies.

The Fed’s structure is designed to balance public accountability with a degree of operational independence. Throughout its history, the Federal Reserve has wielded a lot of power, and has had to thread the needle very carefully. Monetary policy decisions affect the entire economy, and independence has historically allowed the Fed to focus on its dual mandate to the American public: price stability and maximum employment.

But the question of Fed independence has reentered public discussion after recent events, including the DOJ investigation into the Federal Reserve’s building renovations and potential misuse of taxpayer dollars. In another instance, the Supreme Court is deliberating whether Trump’s attempt to fire Fed governor Lisa Cook will stand - a potential departure from the autonomy that the Fed has historically retained. Jerome Powell, current Fed Chair since 2018, has voiced his concerns that these legal battles are a pretext for undermining the Fed’s independence. In a year where we anticipate the appointment of a new Federal Reserve Chair by President Trump, the average investor might wonder:

What does a change in Fed Chair mean for my investment plan?

If you’re a client or have been following us for a while, you know that we’re dedicated to taking the long view - the historical perspective. Leadership transitions at the Fed are not unusual. Since the Federal Reserve was established in 1913, sixteen individuals have served as Chair. Each operated in a different economic and political atmosphere.

Markets don’t just react to what the Fed does - they react to how predictable and transparent the path forward feels. As Fed Chair, Powell has leaned heavily into transparency and forward guidance, which has helped markets form reasonable expectations about where policy may be headed. Similarly, the markets will listen closely to how a new Chair speaks about inflation, growth, and rates. If the messaging feels consistent and grounded in established policy frameworks, investors tend to settle in. If it feels less clear, or the public is anxious about outside interference, the markets might reflect investor confusion as volatility. But as we’ve said before, uncertainty is not an exception in investing: it is the environment. Central banks evolve. Political rhetoric intensifies and fades. The tenure of a Federal Reserve Chair comes to a close, and they are replaced by a new one. And yet over time, businesses adapt, earnings grow, and markets have historically rewarded disciplined, long-term investors.

As financial advisors, we’re watching these and other developments closely - not because we expect dramatic shifts tomorrow, but because our role is to stay informed, measured, and focused on what endures. If and when the underlying conditions change in a way that meaningfully affects risk, return expectations, or portfolio construction, our team will do what we have always done: gauge the situation, communicate with our clients, and move deliberately and intentionally. For now, we believe that staying anchored to the plan is still the best strategy. If recent market or economic news has you wondering whether your plan still fits, that is a worthwhile conversation to have. Let us know, and we would love to schedule a time to chat.